Key Points at a Glance:

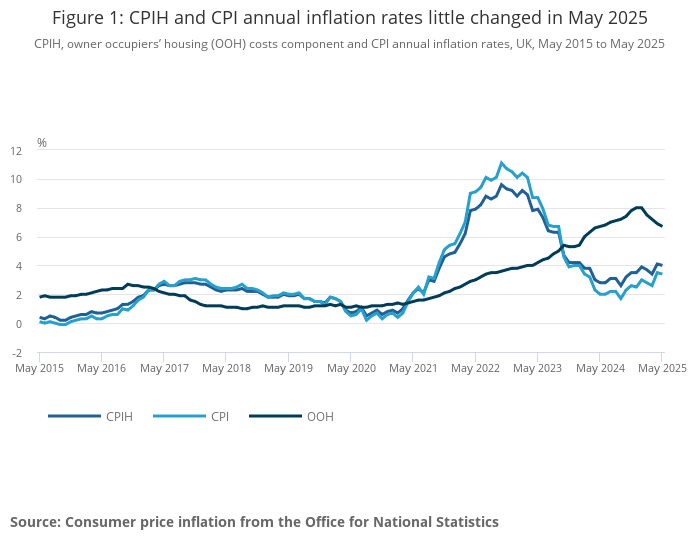

- The Consumer Prices Index including owner occupiers’ housing costs (CPIH) rose by 4.0% in the 12 months to May 2025, down slightly from 4.1% in April.

- The Consumer Prices Index (CPI) also fell marginally, coming in at 3.4% in the 12 months to May 2025, compared to 3.5% the previous month.

- The main contributor to the fall in inflation came from transport, while food and household goods drove inflation upwards.

- Core inflation, which excludes energy, food, alcohol, and tobacco, also fell but remains a concern for policymakers.

A Small Shift, But Not a Turning Point Just Yet

In May 2025, inflation edged down slightly, with the annual CPIH figure moving from 4.1% to 4.0%, and CPI dropping from 3.5% to 3.4%. This means that prices are still rising, just not quite as quickly as they were the month before.

While this is a modest improvement, it’s not enough to suggest a major shift in inflation trends. Core inflation also declined from 4.5% to 4.2% for CPIH, and from 3.8% to 3.5% for CPI,which may offer some encouragement to the Bank of England as it continues to monitor price pressures.

What’s Behind the Numbers?

The change in inflation was shaped by several key areas of spending:

- Transport: This had the biggest impact on bringing the inflation rate down. Prices fell across air fares, road travel, and fuel. The average price of petrol dropped by 2.1p to 132.4p per litre, while diesel fell by 2.6p to 139.1p. Together, this brought annual fuel inflation down to -10.9%. This drop was also influenced by the correction of an earlier error in Vehicle Excise Duty data.

- Food and Non-Alcoholic Drinks: Food prices are still climbing. The inflation rate here increased from 3.4% to 4.4%, the highest level since February. Chocolate, confectionery, and ice cream were among the main contributors, rising due to seasonal sales timing. Meat also became more expensive compared to the same period last year.

- Furniture and Household Goods: Prices in this category also picked up, rising by 0.8% over the year to May. This is a sharp increase from a fall of 0.5% in April. The main drivers were large home items such as fridge freezers, vacuum cleaners, and bedroom furniture, which were recovering from spring sale prices earlier in the year.

- Housing and Household Services: Although still high, inflation here eased slightly from 7.0% to 6.9%. Within this, owner occupiers’ housing costs (which include things like mortgage interest and maintenance) rose by 6.7%, down from 6.9% in April. This remains a significant part of overall inflation, making up over 2 percentage points of the CPIH figure.

Looking Back: Where We’ve Come From

Just a year ago, inflation looked to be under better control. In May 2024, CPIH was at 2.8% and CPI stood at 2.0%, a figure that briefly hit the Bank of England’s target for the first time in years. But since then, inflation has crept up again, driven by persistent wage growth, service sector costs, and underlying price pressures.

It’s worth noting that a data error in April related to car tax (Vehicle Excise Duty) slightly overstated last month’s inflation rates. While that doesn’t change the overall picture dramatically, it does mean that the easing seen in May may be slightly less encouraging than it appears at first glance.

How Might This Affect Interest Rates?

The Bank of England’s next move on interest rates will depend heavily on whether inflation continues to fall and by how much. At present, the base rate remains at 5.25%, a level that has been held steady for some time.

Even though headline inflation has eased slightly, core inflation is still too high for comfort. Services inflation (linked closely to wages) is also proving sticky. Until these areas come down further, it’s unlikely that the Bank will feel confident enough to lower rates.

There is still some speculation that a rate cut could happen later this summer if inflation continues to fall. However, any decision is likely to be cautious, especially with the added backdrop of political change and uncertainty following the recent general election.

What It Means for You

If you’re a homeowner or looking to get on the property ladder, these inflation figures matter. Interest rates are closely linked to inflation, so any future mortgage deals whether fixed or variable will depend on how the economy continues to behave.

While inflation has cooled slightly, it’s not yet enough to signal that borrowing costs will drop. If you’re on a variable or tracker mortgage, the current rates are likely to hold steady for now. Those looking to remortgage or buy should keep an eye on how inflation and interest rate forecasts develop in the coming months.

Moving Forward: How We Can Help

At Kerr & Watson, we’re here to guide you through the uncertainty. Whether you’re considering locking in a mortgage rate, exploring your protection options, or simply want a clearer picture of what these economic shifts mean for your finances, we can help.

We take the time to understand your individual circumstances and goals, then provide advice that’s tailored to you – not just based on the headlines.

Contact Us for Bespoke Mortgage and Insurance Advice

Economic changes like these are a reminder of how quickly financial conditions can shift. Staying informed is one part of the puzzle – making the right decisions for your situation is another. That’s where we come in.

Get in touch with us to explore how the latest inflation and interest rate news could impact your mortgage or insurance planning.

Data Source: Office for National Statistics (ONS) Read more: Consumer price inflation, May 2025