How to Get SA302 Tax Calculations & Tax Year Overviews for Your Mortgage

Get your Tax Calculations and Tax Year Overviews for 2026

If you are self-employed or a limited company director, mortgage lenders nearly always require you to provide your SA302 (Tax Calculations) & Tax Year overviews to support and evidence the income you have earned and declared for your employed, self-employed, dividend and property related remuneration.

Need your Tax Calculations and Tax Year Overviews for your 2026 mortgage? Learn how to access them below, or talk to an adviser for assistance.

Follow the link ‘Get SA302 Tax Calculation for tax year 20xx to 20xx’

Click ‘View your Calculation’

Scroll to the bottom of the page

Click ‘View and print your calculation’

Select ‘Save as PDF‘

Step By Step To Obtain Your Tax Overview

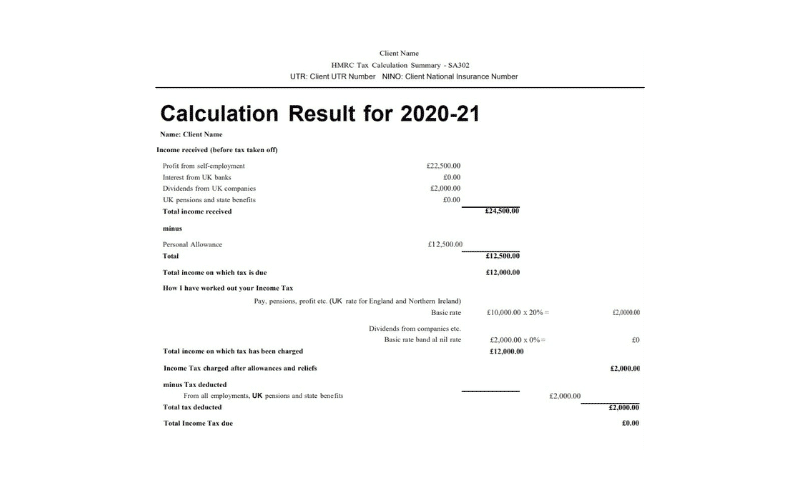

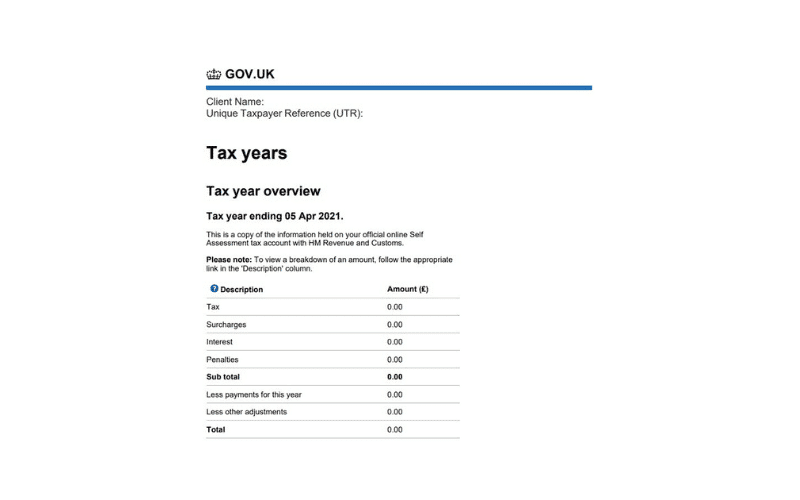

An additional HMRC online document called a Tax Year Overview will be required to verify that the SA302 information is correct, whether you are using online or paper-based SA302s.

The Tax Year Overview is produced by HMRC after you have has submitted your self-assessment tax return. It shows the amount of tax due to be paid directly to HMRC or any available amount for a refund for a given tax year.

In short, these documents help prove your income is stable, reliable and properly declared, this is essential for a self-employed mortgage application.

How Many Years of SA302s Do Lenders Typically Ask For?

Most lenders request:

The last 2 years of SA302s and Tax Year Overviews

Some may ask for 3 years

A small number of specialist lenders may consider just 1 year

The more consistent your income appears, the stronger your application tends to be.

If your income has increased significantly in the latest year, some lenders may use the most recent figure, but others may average the last two years instead. Because criteria varies, it’s important to check which lenders are most suitable before submitting documents.

Alternative Ways to Get These Documents – Use an Accountant

If you’re struggling to download your SA302 or Tax Year Overview directly from HMRC, if you use an accountant, they can usually:

Generate an SA302 directly from HMRC-recognised software

Provide an accountant’s tax calculation summary

Some lenders accept accountant-generated documents, while others prefer them downloaded directly from HMRC. It’s always worth checking first.

Common Errors & Red Flags to Avoid

Submitting the wrong version of these documents can delay your mortgage application. Here are the most common mistakes we see:

Mismatch Between SA302 & Tax Year Overview

The income figure on your SA302 must match the income shown on your Tax Year Overview for that same tax year. If they don’t match, lenders may:

Pause the application

Request clarification

Decline the case until resolved

Always double-check both documents align before sending them.

Printing or Downloading Incorrectly

Common issues include:

Missing pages

Cropped PDFs

Screenshots instead of full downloads

Poor quality scans

Lenders need full, clear documents, not partial screenshots.

Missing HMRC Branding or Reference

Some lenders require:

The HMRC logo

Unique tax reference (UTR)

Submission confirmation details

If these are missing, documents may be rejected.

Need Help Before You Submit These?

Self-employed mortgage applications can become delayed or declined simply because the wrong documents were uploaded. If you’re unsure whats required, which income figure the lender will use or whether your documents will be acceptable.

We can review everything before submission and guide you towards the lenders most likely to accept your income structure. Talk to us today!

Why Kerr & Watson?

Understanding

We take the time to understand your situation so that we can search for the most suitable mortgage and insurance for you. Any recommendation made is completely bespoke to your circumstances.

Experience

Mortgage and insurance advice is our speciality. We have decades of combined experience giving us the knowledge to overcome challenges and find the appropriate solution for your needs.

Communication

We work around your schedule to arrange a mortgage or insurance policy that suits your needs. You’ll be kept updated throughout the entire process with clear communication so you’ll always know what’s going on.

Marie Kitchen was absolutely fabulous. We had an incredibly complicated case due to living abroad and a few hiccups along the way. Marie was persistent and helped us to resolve these efficiently. Highly recommend.

Posted on Google

Michelle

8 June 2026

My 2nd time dealing with Kerr & Watson and they didn't disappoint, great service, professional and patient - big shout out to Andreea & Stephen

Posted on Google

Sean Turner

2 June 2026

I had an excellent experience with Kerr and Watson and would happily recommend them.

A special mention has to go to James, who provided exceptional service throughout. He was professional, approachable, clear in his communication and always willing to help. His support made a huge difference, and we genuinely couldn’t have done it without him.

I would not hesitate in recommending K&W to any family or friends.

Posted on Google

Jackie

15 May 2026

Brad was quick with getting me the right mortgage insurance prior to a move abroad. Polite and professional. Also liked that he would call to remind me take any actions if I hadn't responded to emails

Posted on Google

Ade Kunle

1 May 2026

I will always recommend Kerr & Watson to friend and family.

Posted on Google

Minzel 33

23 April 2026

This is my second product with Matthew, securing a BTL for my LTD with the best rate on the market. Once again great support, guidance and smooth process. Highly recommended, knowledgeable team. Reliable service.

Posted on Google

Freya B

14 April 2026

The team at Kerr & Watson were brilliant end to end. Daniel explained everything clearly, was always available to answer questions and helped us secure a great mortgage rate. The mortgage broking service they offer is worth every penny and I'd not hesitate to use them again. Thank you!

Posted on Google

Dean Langton

7 April 2026

Excellent service and very nice people.

Would highly recommend using them.

Posted on Google

Sat Jakhu

2 April 2026

Great service , efficient and proactive to ensure solutions were right for each property. Always prompt with information and any communication required. Definitely recommended as an organisation who can provide tailored solutions for individual needs.

Awards & Recognition

Contact Us

Free initial conversation. No obligation.

Not ready to apply yet? That’s fine — we can start with a quick conversation about your options.

We aim to respond within a few hours during working days.

By submitting this form you agree that Kerr & Watson may contact you regarding your enquiry.

Your information will be handled in accordance with our Privacy Policy.

Frequently Asked Questions

▸ ▾Do I count as self-employed?

You’re generally considered self-employed if:

You are a sole trader,

You are a partner in a business on a self-employed basis,

You own 20%–25% or more of a limited company that pays you (for example via salary and dividends),

You are a partner in a limited liability partnership (LLP).

Most lenders will treat you as self-employed if your income mainly comes from your business rather than from PAYE with a traditional employer.

▸ ▾self-employed people have to pay higher mortgage rates?

Not automatically. If you can evidence your income and show that the mortgage is affordable, you should have access to the same rates as someone in full-time PAYE employment.

Your rate is more likely to be driven by:

Deposit size / loan-to-value,

Credit profile and conduct (including recent bank statements),

▸ ▾How will a lender calculate my income for a mortgage if I am self-employed?

It depends how you trade:

Sole traders / partnerships: Lenders usually look at your net profit (total taxable income) and average this over the last 2–3 years.

Limited company directors: Lenders may use salary + dividends, or sometimes your share of the company’s net profit. That choice can make a big difference in how much you can borrow. See Can You Get a Mortgage Using Dividends?

Contractors: Some lenders work off a “day rate × number of days per week × 46/48 weeks” rather than just last year’s tax return, especially if you have a strong contract history. More on this in Contractor Mortgages.

If your income dipped recently, some lenders will base affordability on the lowest year, not the average.

▸ ▾How much can a self-employed person borrow for a mortgage?

Most self-employed applicants fall into the same broad range you’ll see quoted online: roughly 4.5× annual income.

However:

Strong, stable income and low personal debt can sometimes push affordability higher with certain lenders.

Irregular or recently increased income can pull it lower.

You can use our Mortgage Calculator for an indication, but the lender’s affordability assessment is what really matters.

▸ ▾Can you get a mortgage with only 1 year of self-employment?

It can be possible with certain lenders.

Typical expectations are:

At least 12 months of trading,

Proof that you’ve worked in that same line of work before going self-employed (for example, you went from PAYE electrician to self-employed electrician),

Strong projected sustainability.

Be prepared to provide more context on your background and current pipeline of work. If you’re newly self-employed on contracts, see: Contractor Mortgages.

▸ ▾How much deposit do you need if you’re self-employed?

In many cases, the minimum deposit is still around 5% (95% loan-to-value), just like an employed applicant.

However, if you have:

Only one year of accounts,

Recent income volatility,

Adverse credit,

…then a larger deposit can help.

If you’re struggling to save a deposit at all, you may find some options in No-Deposit Mortgage.

▸ ▾Can a sole trader get a mortgage?

Yes. As a sole trader, the lender will usually assess you based on your taxable income (net profit) shown on your SA302s / tax calculations, plus your recent business bank activity for consistency.

You’ll normally be asked to show at least two years of figures, but some specialist lenders will consider one.

▸ ▾Can you get a mortgage with an irregular income?

Yes, irregular or seasonal income does not automatically mean “no”.

Mortgage underwriters mainly want to answer two questions:

Is this income real and provable?

Is it likely to continue?

They’ll check business trends, contracts, bank statements, and personal spending.

For how underwriters think, see: The Mortgage Process: What Lenders Look For and What Underwriters Do and What Do Mortgage Lenders Look for on Bank Statements?

This is particularly relevant for people like influencers, content creators, performers and celebrities.

▸ ▾Can you get a mortgage if you work as a contractor?

Yes, contractors can absolutely get mortgages, but it’s more specialist.

Key factors lenders look at:

How long you’ve been contracting,

Length of your current contract and likelihood of renewal,

Your day rate or agreed fixed term,

Gaps between contracts.

Some will lend after as little as 6 months’ continuous contracting; others want 12+ months.

▸ ▾Can you get a mortgage if you work through an agency?

Agency workers can be approved, including temps, supply workers and locum-style roles.

Many lenders like to see a 12-month work history in the same line of work, or evidence of continuous/repeat placements. Some will allow shorter histories or brief gaps if the overall income pattern is strong.

▸ ▾Can I apply for a mortgage while my income is mainly dividends or retained profit?

In many cases, yes.

Some lenders will assess company directors on salary + dividends only. Others will consider retained profit / net profit within the business, which can increase how much you can borrow if you keep income inside the company for tax efficiency.

▸ ▾Will having children affect how much I can borrow if I’m self-employed?

Potentially, yes. Children (or any financial dependants) increase your monthly outgoings. Lenders build those costs into affordability, which can reduce the maximum loan size even if your turnover is strong.

This is especially relevant for self-employed applicants whose income looks high “on paper” but whose disposable income is tighter in reality.

▸ ▾Do I need anything in place before I make an offer on a property?

Yes. Two key steps:

Decision in Principle (also called Agreement in Principle / Mortgage in Principle): This is what most estate agents will ask for before accepting an offer. It shows that a lender has reviewed your basic info and is willing, in principle, to lend. See: Do I Need a Decision in Principle to Make an Offer?

▸ ▾Why should I use a mortgage advisor who specialises in self-employed cases?

Lenders all treat self-employed income differently. The “wrong” lender might only use part of your income (e.g. just salary, not dividends), which can slash how much you’re allowed to borrow.

A specialist self-employed mortgage adviser like Kerr & Watson:

Matches your profile to lenders who understand it,

Prepares your documents so underwriting goes more smoothly,

Shields you from unnecessary declines that could leave a mark.