Inflation – September 2025 At a glance

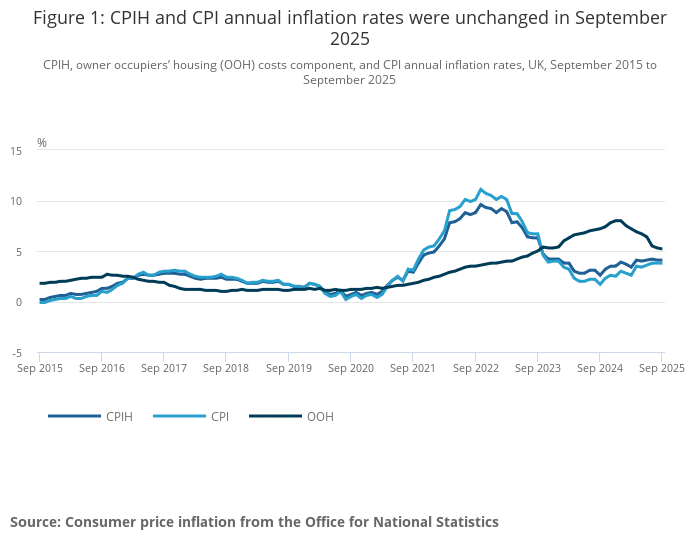

The annual rate of inflation, measured by the Consumer Prices Index (CPI), stood at 3.8 % in the 12 months to September 2025 – unchanged from August.

On a monthly basis, the CPI registered 0.0 % growth in September, meaning prices overall did not rise compared to August.

Underlying or “core” inflation (stripping out food, energy, alcohol and tobacco) edged down to 3.5 % in the year to September, slightly easing from earlier months.

What’s driving (and offsetting) the figures

Transport and fuels

Transport costs pushed upward: annual inflation in transport rose to 3.8 % in September from 2.4 % in August, driven by higher petrol and air-fare costs.

Within transport, motor fuel prices fell by 1.2 % over the year to September, which is a smaller drop than in prior months – meaning fuel still weighs on overall inflation.

Air fares fell between August and September, but because they fell less steeply than a year ago, they still contributed upwards to the annual inflation rate.

Food and drink

Good news: food and non-alcoholic beverage prices rose by 4.5 % in the year to September, down from 5.1 % in the year to August. Monthly food costs even fell by 0.2 % in September.

That slowdown helps ease some pressure on household budgets, but food inflation remains well above the 2 % target.

Housing and household services

Costs in this category rose by 7.3 % in the year to September, very slightly down from 7.4 % in August.

Within that, owner-occupiers’ housing costs increased by 5.2 % in the year – the slowest rise in eight months, though still hefty.

Services and goods

Core CPI (excluding food, energy, alcohol & tobacco) was 3.5 % in the year to September, marginally lower than 3.6 % in August.

Inflation for goods rose slightly (2.9 % annual), while services inflation held steady at 4.7 %.

How things compare and what this means

The headline inflation rate of 3.8 % remains significantly above the 2 % target set by the authorities.

Because inflation hasn’t dropped significantly, there’s less room for confidence that costs will ease rapidly. In turn, that affects what you’ll be considering around mortgages and protection.

For mortgage borrowers or those reviewing protection: elevated inflation means the real value of costs (like repayments, insurance premiums) is under pressure. If interest rates stay high, your repayments may remain comparatively expensive.

A fixed-rate mortgage may continue to appeal if you prioritise certainty, especially if you believe inflation and rates may stay elevated for some time. But conversely, if inflation does start easing, variable or tracker deals might become more attractive.

At Kerr & Watson we can walk you through which path makes most sense in your specific situation.

What this means for your mortgage

- If you’re remortgaging: consider how long you want certainty. With inflation still high and the possibility of interest rates holding, locking in might reduce risk.

- If you’re moving home or buying for the first time: budget for an environment where costs (housing, services, food) may stay elevated, meaning you’ll want some headroom in your repayments.

- Regular review is key: with inflation stuck at this level, it’s more important than ever to revisit your mortgage arrangements to make sure they remain fit for purpose.

Looking ahead

While inflation hasn’t increased recently, the pause doesn’t yet signal clear easing. We’ll be watching closely whether services inflation falls further and whether more of the monthly cost categories begin to ease.

Also keep an eye on wage growth, energy/utility cost changes, and housing costs, all of which feed into inflation and can influence interest rate decisions.

If inflation begins to fall more substantially, interest rates could start to drop; but until that downward trend is firmly established, lenders and borrowers may remain cautious.

Conclusion

Inflation held steady at 3.8 % in the year to September 2025, with lower food inflation providing some relief but offset by higher transport and housing-related costs. While this isn’t dramatic, it means the cost of living remains elevated and for mortgage and protection planning you will want to act with clarity and purpose.

At Kerr & Watson we’re here to help you make sense of how today’s inflation backdrop affects your options and to guide you confidently through your decisions. If you’d like to discuss how the latest figures could impact your mortgage or protection needs, please get in touch with our team today.

If you’d like to discuss how the latest changes could affect your mortgage or protection needs, contact our team today.

Read more: Consumer price inflation, September 2025