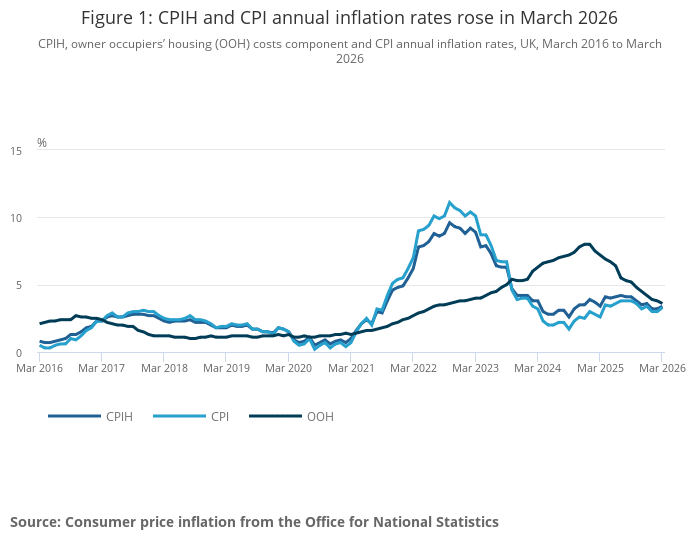

Inflation Update March 2026: CPI Rises to 3.3% as Fuel Costs Drive Increase

Inflation picked up again in March 2026, with the Consumer Prices Index rising to 3.3%, up from 3.0% in February. That means the overall cost of goods and services increased faster than it did the month before, moving further away from the Bank of England’s 2% target.

While the increase is not dramatic, it does show that price pressures have not gone away. Some categories, particularly transport and fuel, pushed inflation higher, while lower clothing prices helped offset part of the rise. For households, this means day-to-day costs are still under pressure, and for borrowers, it is another reminder that interest rate decisions are likely to remain cautious.

Key points at a glance

- CPI rose by 3.3% in the 12 months to March 2026, up from 3.0% in February.

- Monthly CPI rose by 0.7% in March 2026, compared with 0.3% in March 2025.

- Transport made the biggest upward contribution to inflation, with motor fuels playing the largest part.

- Clothing and footwear made the biggest downward contribution, helping offset some of the increase.

- Food prices continued to rise, adding further pressure to household budgets.

- Core CPI, which strips out more volatile items, eased slightly to 3.1% from 3.2%.

- Services inflation rose to 4.5%, showing that underlying price pressures are still present.

What’s driving the numbers

The main reason CPI moved higher in March was a strong rise in transport costs, especially fuel prices. This was supported by smaller upward pressures from food, housing-related costs and some service categories.

At the same time, clothing and footwear prices were weaker than they were a year earlier, which helped limit the overall increase.

This means inflation did not rise because everything suddenly became more expensive at once. Instead, a few key areas made a noticeable difference, particularly those that many households tend to feel quickly in everyday spending.

Transport

Transport was the biggest reason inflation rose in March.

Prices in the transport category increased by 4.7% over the year to March 2026, up from 2.4% in February. On a monthly basis, transport prices rose by 2.4%, which is a sizeable jump.

The biggest factor was motor fuels. Petrol prices rose by 8.6 pence per litre between February and March, compared with a fall of 1.6 pence per litre over the same period last year. The average petrol price reached 140.2 pence per litre in March, the highest level since August 2024.

Diesel saw an even sharper increase. Prices rose by 17.6 pence per litre in March, compared with a fall of 1.6 pence per litre a year earlier. The average diesel price reached 158.7 pence per litre, the highest level since November 2023.

Overall, motor fuel prices rose by 4.9% in the year to March 2026. In February, they had been falling by 4.6% on an annual basis, so this is a clear turnaround.

Air fares also contributed to the rise. Prices increased by 10.0% between February and March, compared with a slight fall during the same period last year. There were also smaller upward effects from vehicle maintenance and repair.

Rail fares, however, provided a small offset, as some fares remained frozen and overall price changes were limited.

Food and drink

Food prices continued to move upwards in March, adding to the pressure many households are already feeling.

Food and non-alcoholic beverage prices rose by 3.7% in the 12 months to March 2026, up from 3.3% in February. On a monthly basis, prices rose by 0.3%, whereas they were broadly unchanged in March last year.

The upward pressure came mainly from chocolate and confectionery, meat, fish and soft drinks. Some of this was offset by weaker price movements in bread and cereals, along with dairy products, but the overall picture is that food inflation is still edging higher rather than easing back.

For you, this matters because food is one of the most visible parts of inflation. Even modest increases can quickly affect monthly budgets.

Housing and household services

Housing and household services also added to inflation, with the annual rate rising to 5.3% in March 2026 from 4.6% in February.

One of the main reasons for this increase was a very sharp rise in domestic heating oil prices. Prices rose by 90.5% in March compared with a fall of 7.5% a year earlier. That pushed the annual rate for domestic heating oil to 95.3%, the highest since September 2022.

Although owner occupiers’ housing costs are part of CPIH rather than CPI, the wider housing and household services category still remains one of the most important contributors to inflation overall. In simple terms, housing-related costs are still playing a big role in keeping inflation above target.

Clothing and footwear

Clothing and footwear helped soften the overall inflation figure.

Prices in this category fell by 0.8% in the 12 months to March 2026, compared with a rise of 0.9% in February. This was the largest downward contribution to the annual CPI movement.

On a monthly basis, clothing prices still rose by 0.6% in March, which is normal as new spring ranges continue to come into shops after the sales period. However, prices rose by much less than they did a year earlier, which is why the annual rate dropped.

The biggest downward effects came from women’s and children’s clothing.

Core inflation

Core CPI excludes energy, food, alcohol and tobacco. It is often watched closely because it can give a better sense of underlying inflation trends without the more volatile categories.

Core CPI fell slightly to 3.1% in March 2026, down from 3.2% in February.

That small fall is worth noting, but it does not suggest inflation is fully under control. Services inflation actually increased from 4.3% to 4.5%, and goods inflation rose from 1.6% to 2.1%. This suggests that while some of the more volatile areas may move around from month to month, broader price pressures are still present.

How CPI compares internationally

Compared with other major economies, inflation remains relatively high.

In March 2026, CPI stood at 3.3%, compared with 2.8% across the EU, 2.8% in Germany and 2.0% in France.

That does not automatically mean the same response is needed everywhere, but it does show that inflation remains more persistent here than in some comparable economies.

What this means for interest rates

With CPI now at 3.3%, inflation is still above the Bank of England’s target. The rise from February to March may make policymakers more cautious about cutting interest rates too quickly.

The slight drop in core CPI is a positive sign, but the increase in headline inflation, rising services inflation and higher fuel costs all point to ongoing pressure in the economy. That means any future rate reductions are still likely to depend on clearer evidence that inflation is moving down in a sustained way.

For you, this means mortgage rates may not fall as quickly as some had hoped. Lenders will continue to price products based on market expectations, swap rates and the wider outlook, so the direction of travel may still be uneven.

What this means for you

If you are planning to buy, remortgage or review your protection arrangements, the latest inflation figures are worth paying attention to.

Higher inflation can affect mortgage affordability, household budgets and the way lenders price risk. Even if base rate changes are gradual, persistent inflation can keep borrowing costs higher for longer than many people would like.

That does not mean you should put your plans on hold. It means you should make decisions based on clear advice and a proper understanding of your options.

If your current deal is ending soon, it may be sensible to start reviewing your mortgage early. If you are buying for the first time, your affordability may look different depending on rates, monthly commitments and how lenders assess your income. If you already own a home, reviewing your protection can also be worthwhile, especially when household budgets are under more strain.

At Kerr & Watson, we help you make sense of what is happening in the economy and what it could mean for your mortgage and protection choices. Whether you are moving home, remortgaging or buying for the first time, you can get straightforward advice tailored to your situation.

Looking ahead

There are a few areas worth watching over the next few months:

- Fuel prices, which had a strong impact on March’s inflation figure

- Food prices, which continue to move upwards

- Services inflation, which remains relatively high

- Future Bank of England decisions on interest rates

If inflation continues to stay above target, rate cuts could remain gradual. If price pressures begin to ease more clearly, the outlook may improve. Either way, it is sensible to stay informed and plan ahead.

Conclusion

CPI rose to 3.3% in March 2026, up from 3.0% in February, showing that inflation has moved higher again rather than continuing to ease. The biggest driver was transport, particularly motor fuels, while falling clothing prices helped offset some of the increase.

For households, this means the cost of living remains an important issue. For borrowers, it means interest rate expectations may stay cautious for now.

By understanding what is happening and reviewing your options early, you can put yourself in a stronger position. At Kerr & Watson, we are here to help you work through your mortgage and protection decisions with clear, practical advice.

If you would like to discuss how the latest inflation figures could affect your plans, get in touch with Kerr & Watson.

Read more: Consumer price inflation, March 2026