Inflation – December 2025 At a glance

Inflation moved slightly higher in December, ending the year with prices rising faster than they were in November. While the increase is modest, inflation remains well above the Bank of England’s long-term target of 2%, which means the cost of everyday living is still a real issue for many households.

The latest figures show that progress on inflation has slowed, and in some areas, pressures are building again. Understanding what is driving these changes can help you make better financial decisions, especially if you are thinking about your mortgage, remortgaging, or future plans.

Key points at a glance

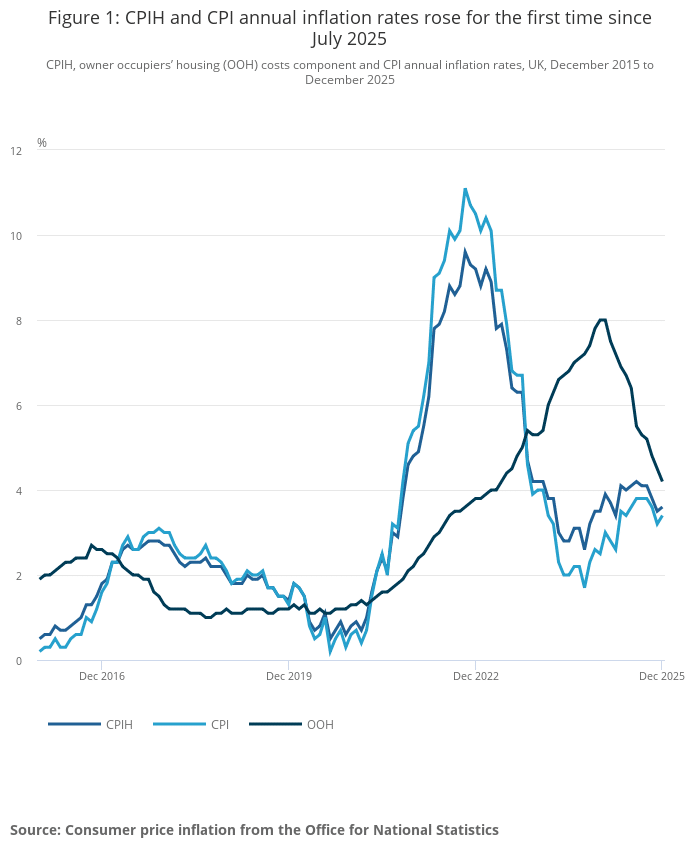

- Consumer Prices Index (CPI) rose by 3.4% in the 12 months to December 2025, up from 3.2% in November.

- On a monthly basis, CPI increased by 0.4% in December, compared with a 0.3% rise at the same time last year.

- Alcohol and tobacco, transport, and restaurants and hotels were the biggest contributors to the increase.

- Food prices continued to rise, adding pressure to household budgets.

- Core CPI remained at 3.2%, showing underlying inflation pressures have not eased further.

What the December CPI figure tells you

CPI is the main inflation measure most people hear about, and it is the one closely watched by policymakers when making interest rate decisions. A rise from 3.2% to 3.4% may seem small, but it marks the first increase after a period of gradual easing.

For you, this means prices are still rising at a pace that is noticeably higher than normal. While inflation is far below the peaks seen in recent years, it has not yet settled back to comfortable levels.

Monthly inflation also picked up slightly, suggesting that price pressures toward the end of the year were stronger than they were in December last year.

What’s driving inflation higher

Several categories pushed inflation up in December. Some of these are seasonal, while others reflect more persistent pressures.

Alcohol and tobacco

Alcohol and tobacco prices rose sharply compared with November.

Prices in this category increased by 5.2% over the year to December, up from 4.0% the month before.

On a monthly basis, prices rose by 1.0%, compared with a fall at the same point last year.

This increase was largely driven by tobacco prices, following changes to tobacco duty late in November. The timing of duty rises can have a noticeable impact on inflation figures, and this was a key factor behind December’s increase.

Transport

Transport costs were another major contributor.

Prices in this category rose by 4.0% over the year, up from 3.7% in November.

Monthly prices increased by 1.3%, higher than the increase seen a year earlier.

Air fares were the biggest factor, rising sharply in December due to travel patterns around the festive period. While fuel prices had only a limited impact, the overall cost of getting from A to B increased, adding to inflation.

Food and non-alcoholic beverages

Food prices remain a challenge for many households.

Food and non-alcoholic beverages rose by 4.5% over the year to December, up from 4.2% in November.

Monthly prices increased by 0.8%, compared with 0.5% a year earlier.

The biggest upward pressures came from staples such as bread, cereals, and vegetables. Even small monthly increases can add up over time, and food remains one of the areas where households feel inflation most directly.

Restaurants and hotels

Eating out and accommodation also became more expensive.

Prices in this category rose by 3.8% over the year, up from 3.5% in November.

On a monthly basis, prices increased by 0.2%.

While not as sharp as food or transport, these costs contribute to the overall picture and reflect ongoing pressures in the service sector.

Areas where inflation eased

Not every category added to inflation.

Housing and household services saw a slight easing in annual price growth.

Prices in this category rose by 4.9% over the year, down from 5.1% in November.

Monthly growth was just 0.1%, lower than the same time last year.

This slowdown is a positive sign, particularly as housing-related costs have been one of the biggest drivers of inflation in recent years. However, prices are still rising quickly, and the level remains high.

Core inflation and what it means for you

Core CPI strips out volatile items such as food, energy, alcohol, and tobacco to give a clearer view of underlying inflation.

Core CPI remained at 3.2% in December, unchanged from November.

This is the lowest level since late 2024, but it has stopped falling.

For you, this suggests that while inflation is no longer accelerating rapidly, it is proving stubborn. Underlying price pressures, especially in services, are still present and could keep inflation higher for longer than previously hoped.

How inflation compares internationally

Inflation remains higher here than in many other major economies.

In December, CPI stood at 3.4%, compared with 2.0% in Germany and 0.7% in France.

This gap highlights why interest rates are likely to stay higher for longer, as policymakers focus on bringing inflation back under control.

What this means for interest rates

With inflation moving up again and core inflation holding steady, there is little immediate pressure on the Bank of England to cut interest rates quickly.

Rates are likely to remain at current levels for some time while policymakers look for clearer evidence that inflation is falling consistently.

For you, this means borrowing costs are unlikely to drop sharply in the short term. Any future reductions are expected to be gradual rather than sudden.

What this means for your mortgage

Inflation and interest rates are closely linked, and both play a big role in mortgage pricing.

If you are on a variable or tracker rate, higher inflation increases the chance that rates will stay where they are for longer.

If you are coming to the end of a fixed rate, mortgage affordability remains an important consideration when choosing your next deal.

If you are buying for the first time or moving home, higher rates mean careful planning is essential to ensure your mortgage remains comfortable over the long term.

While fixed-rate deals can offer certainty, the right choice depends on your circumstances, plans, and appetite for risk.

How Kerr & Watson can help

Economic updates can feel overwhelming, but you do not have to navigate them alone. At Kerr & Watson, you receive clear, straightforward advice tailored to your situation.

You can get help with:

- Understanding how inflation and interest rates affect your mortgage options.

- Reviewing your current deal and deciding whether to fix, track, or wait.

- Planning ahead if your fixed rate is ending in the next 6 to 12 months.

- Making informed decisions that balance certainty, flexibility, and affordability.

Looking ahead

Inflation is likely to remain uneven over the coming months. Areas to watch include:

Food prices, which continue to rise faster than overall inflation.

Transport costs, particularly around travel periods.

Core inflation, which shows whether underlying pressures are easing.

Interest rate decisions, which will respond to these trends over time.

Conclusion

Inflation rose to 3.4% in December 2025, driven by higher transport, food, and alcohol and tobacco prices. While housing-related inflation has eased slightly, overall price pressures remain and progress has slowed.

For you, this means the cost of living remains elevated and interest rates are likely to stay higher for longer. Careful planning and informed advice are more important than ever.

At Kerr & Watson, you can get clear guidance on how these economic conditions affect your mortgage and protection needs. If you would like to review your options or plan your next steps with confidence, get in touch with our team today.

Read more: Consumer price inflation, December 2025